Fresh discussions around artificial intelligence and aging populations are drawing attention to two rapidly emerging global concerns: whether AI can help reduce economic inequality in China and how dementia is increasingly creating financial vulnerability for older citizens. The debate reflects a broader shift in which governments, financial institutions, and technology companies are confronting the social consequences of demographic change and AI-driven transformation.

Recent reporting highlighted how Chinese policymakers and technology leaders are exploring AI as a potential tool to improve productivity, expand access to services, and narrow inequality gaps between urban and rural populations. The conversation comes as China accelerates investment in domestic AI capabilities amid intensifying global competition with the United States.

At the same time, attention has turned toward the growing financial risks associated with dementia, particularly how cognitive decline can lead to poor financial decisions, fraud exposure, and weakened retirement security. Banks, insurers, and healthcare systems are increasingly being pressured to strengthen safeguards for aging populations.

The two issues intersect around a central question facing modern economies: how technology can support vulnerable communities without deepening social and economic disparities.

China’s AI push is unfolding during a period of slowing economic growth, rising youth unemployment, and widening wealth disparities between major urban centers and less-developed regions. Beijing has increasingly positioned AI as a strategic national priority capable of modernizing manufacturing, education, healthcare, and public administration.

Companies such as Alibaba, Tencent, and Baidu have expanded investments in generative AI models, automation systems, and smart-city infrastructure. Chinese policymakers argue that these technologies could improve efficiency and increase access to services in underserved communities.

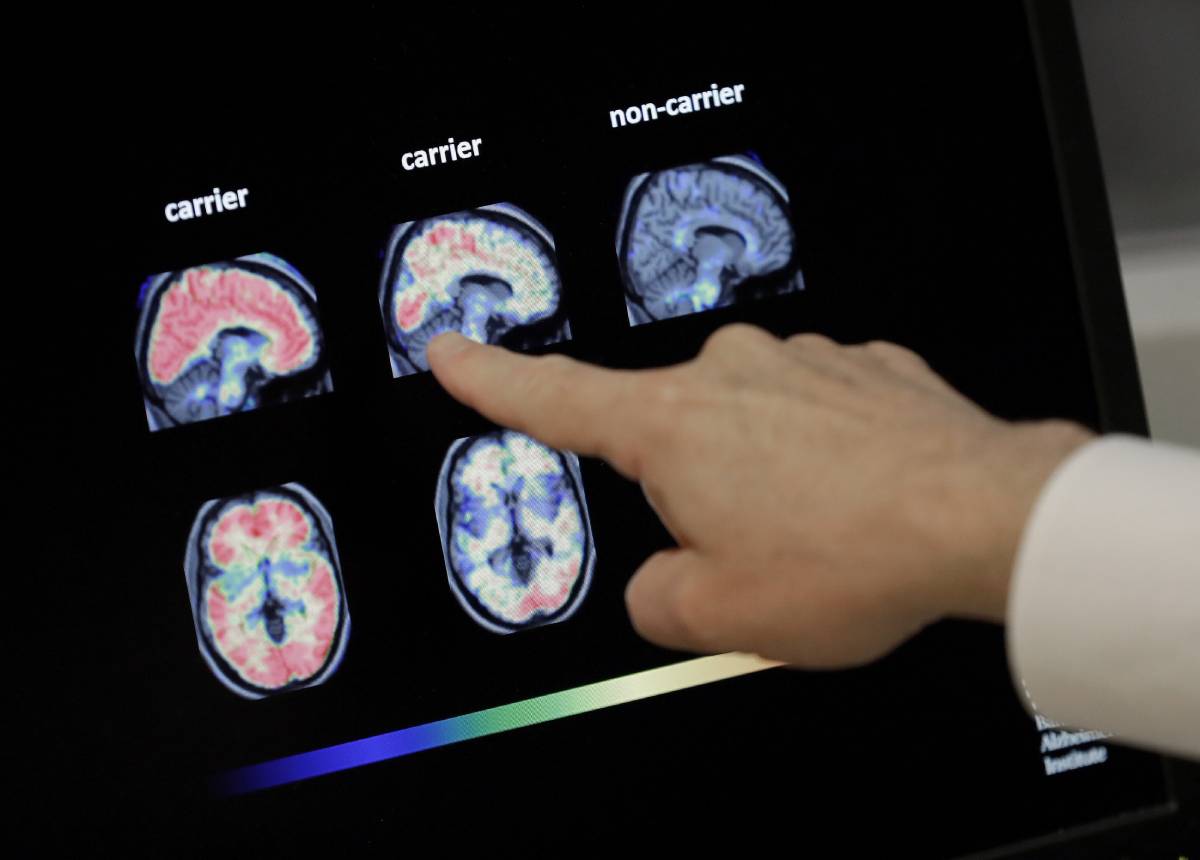

Simultaneously, aging populations are becoming a major economic concern across both developed and emerging markets. Dementia cases are projected to rise sharply over the next two decades, creating new healthcare and financial-management challenges. Financial institutions worldwide are already facing increased scrutiny over elder fraud prevention, cognitive health protections, and digital banking accessibility.

The intersection of AI adoption and demographic pressure reflects a wider global trend in which technology is increasingly expected to address structural social issues once managed primarily through public policy and welfare systems.

Economists and technology analysts remain divided on whether AI can genuinely reduce inequality or whether it could instead widen income gaps by disproportionately rewarding highly skilled workers and large corporations. Some experts argue that AI-driven automation could improve access to education, healthcare diagnostics, and financial services in underserved regions, particularly in developing economies.

Others caution that unequal access to computing infrastructure, data resources, and digital literacy may reinforce existing disparities. Analysts note that the benefits of AI often concentrate among companies and regions with strong capital access and advanced technological ecosystems.

Healthcare specialists and banking experts have also raised concerns about the financial consequences of dementia. Researchers increasingly warn that cognitive decline often begins affecting financial judgment years before formal diagnosis, leaving individuals vulnerable to scams, impulsive spending, or poor investment decisions.

Financial institutions are responding by exploring AI-powered fraud detection tools, behavioral monitoring systems, and enhanced consumer protections for elderly clients. However, privacy advocates warn that such systems must balance safety with individual autonomy and data protection standards.

Industry observers say the broader conversation highlights how AI is no longer viewed solely as a productivity tool, but as a mechanism with direct societal and ethical implications.

For businesses, the developments reinforce the need to integrate social responsibility into AI deployment strategies. Financial institutions, insurers, healthcare providers, and technology firms may increasingly be expected to design products that account for aging populations and cognitive health vulnerabilities.

Investors are also paying closer attention to companies developing AI solutions for elder care, financial monitoring, healthcare analytics, and social infrastructure. The aging economy is emerging as a significant long-term market opportunity.

Governments may face growing pressure to establish clearer regulations governing AI ethics, elder financial protection, healthcare privacy, and algorithmic accountability. Policymakers in both China and Western economies are likely to accelerate discussions around inclusive AI growth models that balance innovation with social stability. For executives, the broader challenge lies in ensuring that AI adoption strengthens resilience and accessibility rather than amplifying economic fragmentation or consumer risk.

Attention will now focus on how governments and corporations translate AI ambitions into measurable social outcomes. In China, policymakers are expected to continue framing AI as a strategic tool for economic modernization and national competitiveness.

Meanwhile, financial institutions and healthcare providers worldwide will likely intensify efforts to protect aging consumers from cognitive-related financial harm. The wider uncertainty remains whether technology can effectively narrow inequality gaps while preserving trust, privacy, and social stability in increasingly digital economies.

Source: NPR

Date: May 12, 2026